On the Hook

Here’s the promised graph, explained below:

Fishing for Complements

Robert Solow (1987) pointed out that “a technological revolution, a drastic change in our productive lives” had curiously been accompanied by “a slowing-down of productivity growth, not by a step up.” His famous productivity paradox, that one “can see the computer age everywhere but in the productivity statistics,” named a challenge for economists seeking to reconcile the emergence of exciting technological breakthroughs with tepid productivity growth (Brynjolfsson 1993).

Solow’s Paradox was not unique. In this paper, we argue it was one example of a more general phenomenon resulting from the need for intangible investments in early stages of new general purpose technologies. General purpose technologies (GPTs) are “engines for growth.” Specifically, they are pervasive, improve over time, and lead to complementary innovation (Bresnahan and Trajtenberg 1995). However, along with installing more easily measured items like new types of physical equipment and structures, we emphasize that realizing their potential also requires large intangible investments and a fundamental rethinking of the organization of production itself. Firms must create new business processes, develop managerial experience, train workers, patch software, and build other intangibles. This raises productivity measurement issues because intangible investments are not readily tallied on a balance sheet or in the national accounts.

The presence and timing of this sort of intangible investment is one reason why Solow’s Paradox could occur. When a new GPT emerges, there will be a period, possibly of considerable length, during which measurable resources are committed, and measurable output forgone, to building new, unmeasured inputs that complement the GPT.2 For example, the technologies driving the British industrial revolution led to “Engels’ Pause,” a half-century-long period of capital accumulation, industrial innovation, and wage stagnation (Allen 2009; Acemoglu and Robinson 2013). In the later GPT case of electrification, it took a generation for the nature of factory layouts to be re-invented in order to fully harness the new technology’s benefits (David 1990). Solow highlighted a similar phenomenon roughly two decades into the IT era.

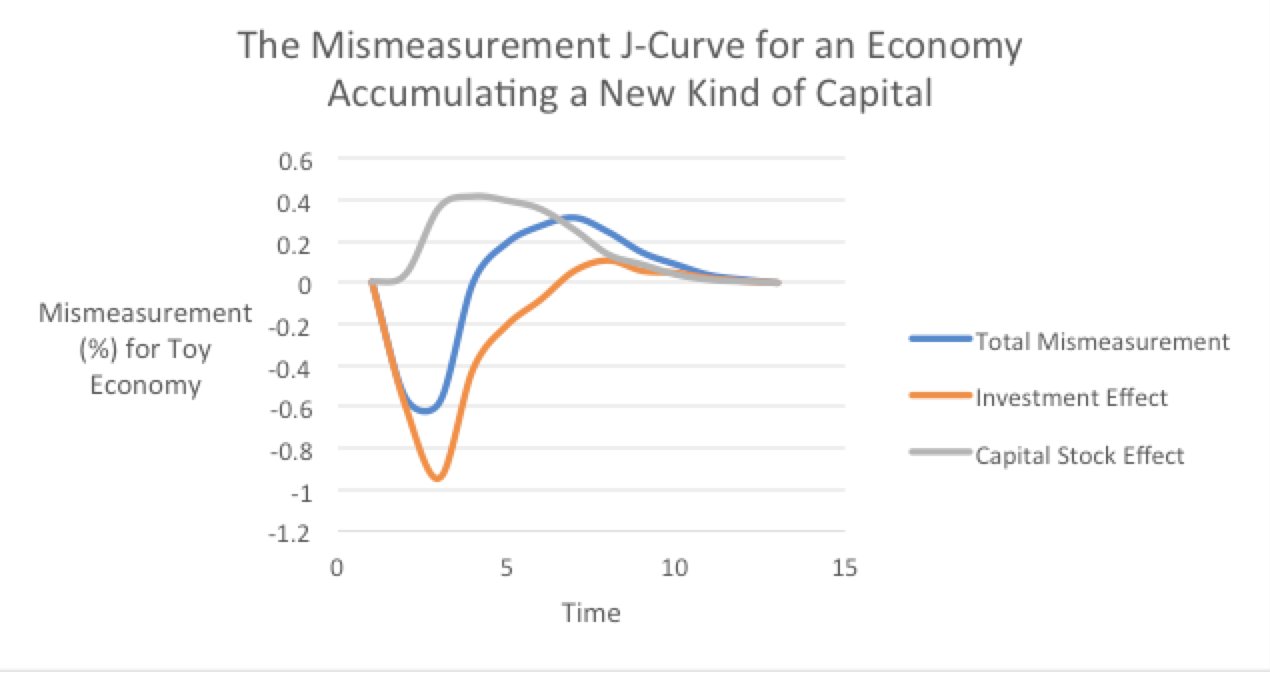

We call the measurement aspect of this phenomenon the Productivity J-Curve. As firms adopt a new GPT, total factor productivity growth will initially be underestimated because capital and labor are used to accumulate unmeasured intangible capital stocks. Later, measured productivity growth overestimates true productivity growth because the capital service flows from those hidden intangible stocks generates measurable output. The error in measured total factor productivity growth therefore follows a J-curve shape, initially dipping while the investment rate in unmeasured capital is larger than the investment rate in other types of capital, then rising as growing intangible stocks begin to contribute to measured production. In the long run, as intangible investments and capital stocks reach their steady-state growth rates, the return-adjusted value of the unmeasured intangible capital stock service flows (in expectation) approaches the value of the initial unmeasured investment. This means that some of the mismeasurement effects on productivity growth can persist even in the long run.

Erik Brynjolfsson, Daniel Rock and Chad Syverson – The Productivity J-Curve: How Intangibles Complement General Purpose Technologies (NBER Working Paper 2018, revised 2020)